Why Your Credit Score Matters More Than You Think

Imagine walking into your dream condo, only to be told your application is denied. Or getting slapped with a sky-high interest rate on a car loan. Sounds brutal, right? That’s the power of your credit score—a tiny three-digit number that can make or break your financial future.

A credit score isn’t just some random number; it’s your financial reputation in Canada. And here’s the kicker: 59% of Canadians don’t know their credit score. Don’t be part of that statistic. It determines whether you can borrow money, how much you can borrow, and how much interest you’ll pay. The higher your score, the better your financial opportunities.

Let’s break it all down—what your credit score is, why it matters, and, most importantly, how to improve it.

What is a Credit Score?

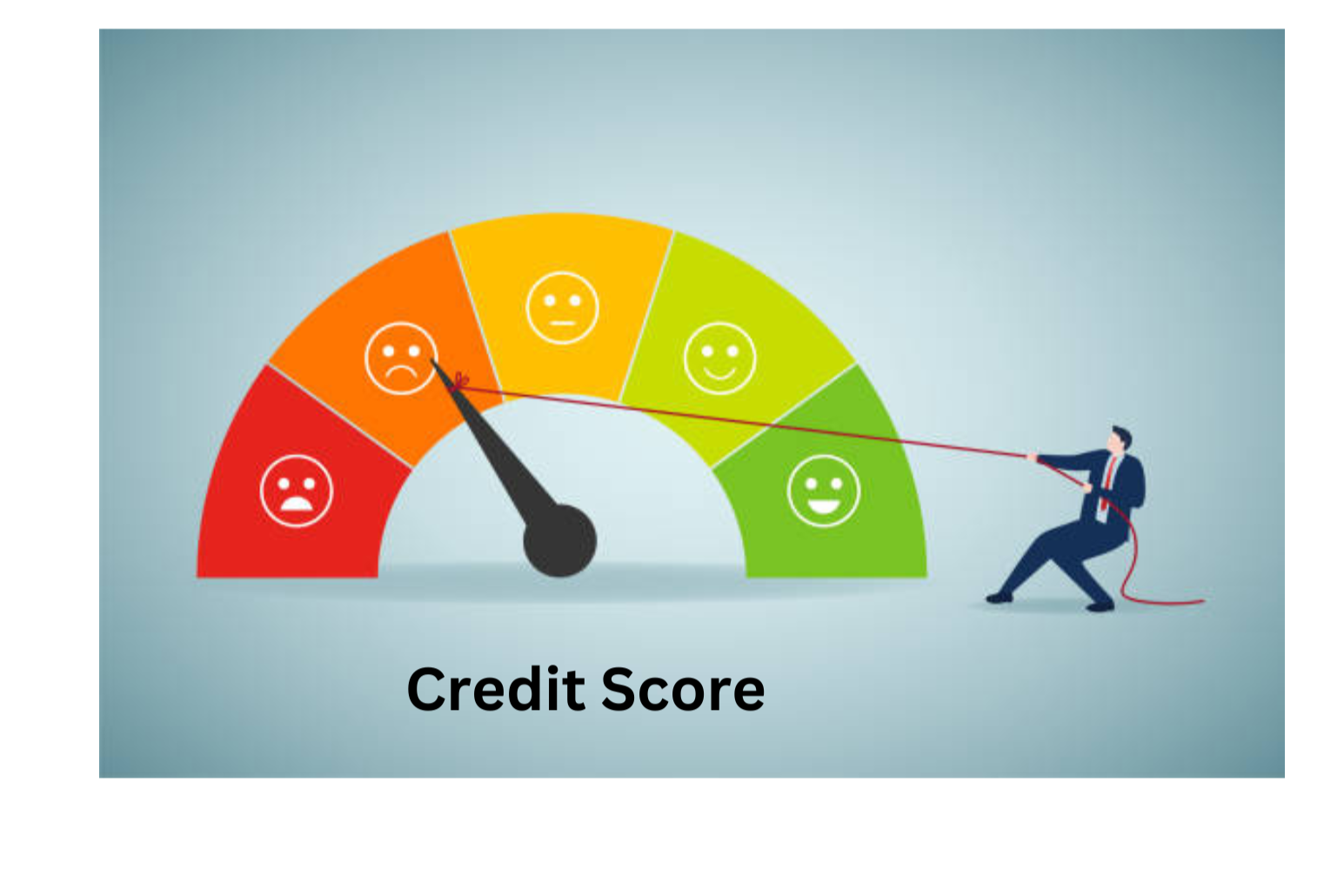

Your credit score is a number between 300 and 900 that represents how responsible you are with credit. Think of it as a report card for your financial habits. The higher the score, the lower the risk for lenders. It’s based on your credit history and is used by banks, landlords, and even some employers. Here is a breakdown of what the number means:

Credit Score Ranges in Canada

- 300-559: Poor (You’ll struggle to get approved for credit.)

- 560-659: Fair (You may get credit, but with high-interest rates.)

- 660-724: Good (Most lenders will approve you.)

- 725-759: Very Good (You’ll get better interest rates.)

- 760-900: Excellent (You’ll get the best offers and the lowest rates!)

Who Determines Your Credit Score?

In Canada, two major credit bureaus—Equifax and TransUnion—calculate your credit score. Each one uses slightly different models, so your score may vary slightly between them.

Lenders, like banks and credit card companies, report your payment history and credit usage to these bureaus. Then, the bureaus crunch the numbers to generate your score.

What Factors Affect Your Credit Score?

Your credit score isn’t random—it’s based on five key factors:

- Payment History (35%) Did you pay your bills on time? Late or missed payments can seriously damage your score.

- Credit Utilization (30%) How much of your available credit are you using? Using more than 30% of your credit limit can lower your score. This means if you have a credit card with a limit of $10,000, keep that balance below $3,000.00

- Credit History Length (15%) How long have you had credit accounts open? The longer, the better.

- Credit Mix (10%) A mix of different types of credit—credit cards, loans, mortgages—can help improve your score.

- Hard Inquiries (10%) Every time you apply for credit, a “hard inquiry” is made. Too many inquiries in a short period can lower your score.

Why Does It Matter?

Your credit score isn’t just about borrowing money. It’s a key factor in many life decisions. Landlords check it before renting to you. Employers might review it during hiring. Even cell phone providers use it to determine if you qualify for a plan. A low score can mean higher interest rates or outright rejection. A high score? It opens doors.

How to Check Your Credit Score for Free

You can check your credit score for free using services like:

- Equifax Canada (free report once per year)

- TransUnion Canada (free report once per year)

- Borrowell (free ongoing score tracking)

- Credit Karma (free ongoing score tracking)

How to Improve Your Credit Score (Fast!)

If your credit score isn’t where you want it to be, don’t panic! Here’s how to fix it:

- Pay Bills on Time Even one missed payment can drop your score. Set up automatic payments to avoid this.

- Keep Credit Utilization Low Try to use less than 30% of your total credit limit. If your limit is $10,000, aim to keep your balance below $3,000.

- Avoid Opening Too Many New Accounts Each new credit application can temporarily lower your score. Only apply for credit when necessary.

- Don’t Close Old Accounts The longer your credit history, the better. Even if you’re not using a card, keeping it open can help your score.

- Check Your Credit Report Regularly Errors happen. Request a free credit report from Equifax or TransUnion annually to ensure everything’s accurate. Mistakes happen! If you find an error, contact Equifax or TransUnion to get it corrected.

How Long Does It Take to See Credit Score Improvements?

- 30-60 days: Minor changes (paying down balances, correcting errors)

- 3-6 months: Moderate improvements (consistent payments, lower credit usage)

- 12+ months: Major score recovery (building long-term positive history)

Conclusion: Take Control of Your Financial Future

Your credit score isn’t just a number—it’s the key to lower interest rates, better financial opportunities, and more peace of mind. Whether you’re buying a home, financing a car, or just want to keep your options open, improving your credit score is one of the smartest financial moves you can make.

Start today—check your score, make small changes, and watch your financial future brighten!

Next blog ….. How to Manage Debt

Leave a Reply to Struggling with Debt? These Tips Will Help You Manage It and Regain Control – Let’s Get Smarter With Money!Cancel reply